Health Care Should Get "Smart" about Protecting Patient Data

Kim BellardAdmit it: you're worried about your online privacy. Admit it: your personal health information is one of the things you worry most about getting hacked. Admit it: you don't understand why your health care providers seem to have a hard time sharing key information about you. And admit it, you're not quite sure what health insurers really do, except for always saying no and for getting between you and your health care providers.

Kim BellardAdmit it: you're worried about your online privacy. Admit it: your personal health information is one of the things you worry most about getting hacked. Admit it: you don't understand why your health care providers seem to have a hard time sharing key information about you. And admit it, you're not quite sure what health insurers really do, except for always saying no and for getting between you and your health care providers.

This is why blockchain is the new hope -- or hype -- for health care. What intrigues me most about it, though, are its "smart contracts."

The GAO recently cited health as a key area of cybersecurity weakness, and TrendMicro profiled why cybercrime is a particular threat for health care. The 2017 Xerox eHealth Survey found that 44% of Americans were worried about their personal health information being stolen, and one has to wonder if the other 56% are asleep or just don't care.

So it is no wonder that blockchain, with its touted higher level of security, is the new darling for health care pundits.

A previous post attempted to convey the blockchain basics and the hype (some of which interested readers were quick to try to deflate). A recent article in NEJM Catalyst attempted to "decode" the hype, analyzing both the potential applications of blockchain in health care and the some of the challenges it would face. The authors warned that:

the challenges and realities of health care and health care data may be insurmountable — even as some argue that blockchain could revolutionize how we share health care data.

The financial service industry, for one, is paying attention to blockchain. A consortium of big banks and tech companies just announced a consortium to expand blockchain technology. Improved security would be nice, but what may be catching their eyes most is the prospect for saving money.

Accenture estimated that blockchain could reduce investment bank's infrastructure costs by 30%, some $8b - $10b annually for the 10 largest such banks. It could slash the cost for many back office functions, such as reporting, compliance, and clearance/settlement.

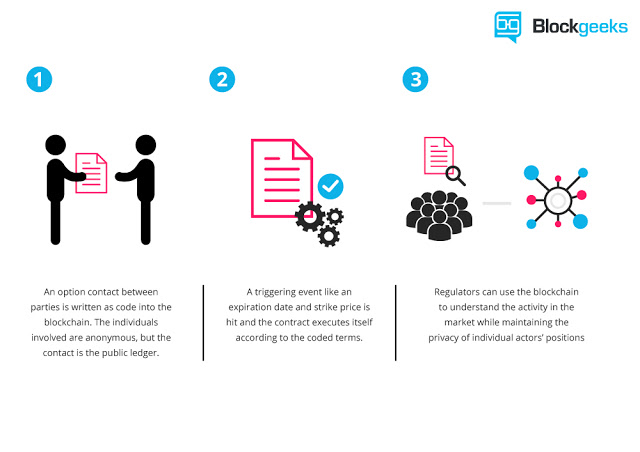

Smart contracts are one of the features blockchain offers to help achieve these savings. Smart contracts are, essentially, automated programs that self-execute and self-enforce, based on satisfaction of the underlying terms. They can work between two parties, or for complex multi-party agreements, and do so without any middlemen -- no lawyers or other third parties.

Smart contracts have been compared (for better or worse) to a vending machine: put your money in, get your desired choice out. Nick Szabo, who may or may not have invented Bitcoin, uses the vending machine analogy, and elaborates:

Think of blockchain as an army of robots checking up on each others' work. Where traditionally you have accountants and lawyers, there are now a wide variety of things we can do with the vending machine-like mechanism to replace the job of traditional contracts plus added cryptographic mechanisms for integrity."

Electronic health records and exchange of patient data more generally are often cited as obvious potential uses for blockchain in health care, as the data is not stored in silos and can be shared by trusted partners. Those may prove valid uses, but blockchain's killer app may be smart contracts -- such as to cut out health plans.

You get services from your health care provider, but your health plan decides if your contract covers the care, and how much, if any, it will pay towards the care. Your provider may or may not be in your health plan's network, they may or may not have to contact your health plan for "permission" for some services, may or may not submit a claim on your behalf, and may or may not receive payment directly from them (as well as from your for your portion).

So, yes, they are in the middle.

Your health plan is really a contract between you and your health insurer. If you pay the required amount, they are obligated to provide payment for a specified set of health care services -- under a specified set of conditions: application of deductibles/coinsurance/copayments, use of provider networks, limits on certain services, medically necessity, excluded services, etc. Like many insurance contracts, to understand it you probably need a law degree.

Imagine a smart contract between you and your doctor. She promises to, say, fix your broken leg and, if she does, you promise to pay her $X. The two of you would agree how and when to decide if the leg is, in fact, fixed. All that goes in the smart contract.

No ICD-10 or CPT codes, no unknown charges, no payment for care that doesn't work; just mutual agreement about what each party will do. You fund a virtual currency account, she provides the services, the smart contract monitors when the conditions are met, and issues payment once they are.

None of that looks like the current health care system.

The broken leg is, admittedly, a relatively simple example, and even it would require some work to define the contract. How badly is the leg broken? How do you know if the price is reasonable? How do you evaluate if the leg is fixed to your satisfaction? And all this is supposed to happen while you are in pain in the ER or doctor's office?

However, none of that is insurmountable, nor alien to advocates of reference pricing or value-based care. Defining expectations about care, price, and outcomes prior to receipt of care would be a real change, but one that would go a long way to changing the way our health care system works.

It is easiest to see smart contracts working for conditions with clear expected outcomes, costs that are relatively affordable, and between two parties. However, they don't have to be so limited, and could be designed for use with multiple parties, be they multiple providers or multiple funding sources (e.g., using a Kickstarter campaign or even a catastrophic health plan).

Blockchain may prove to not fit the structure we've evolved in health care. Smart contracts may not be made smart enough to understand what happens in our health care system. But maybe, just maybe, blockchain could be the next big thing in health care, and smart contracts may be its killer app.

| Health Care Should Get "Smart" was authored by Kim Bellard and first published in his blog, From a Different Perspective.... It is reprinted by Open Health News with permission from the author. The original post can be found here. |

- Login to post comments