Kangaroos, Insurance Companies, and the Rising Cost of Healthcare

Kim BellardLet's start with a joke:

Kim BellardLet's start with a joke:

A kangaroo walks into a bar, puts down $20, and orders a beer. The bartender figures that a kangaroo probably doesn't really understand money, so he gives the kangaroo the beer but only a dollar in change. He casually observes: "we don't get too many kangaroos in here." The kangaroo replies: "With these prices, no wonder."

My friends, we are that kangaroo, and health care is that bar. Only we keep going back to it.

Complaining about health care prices is nothing new. The medical component of CPI has been higher than the overall CPI for decades. As far back as 1989 Gerry Anderson and colleagues showed "It's the Prices, Stupid" that explained why our national spending was so high compared to other countries.

More recently, Elizabeth Rosenthal detailed those prices in an series of reports in The New York Times. She recently followed those up with her incisive book An American Sickness. Dr. Rosenthal also illustrated some of the clever techniques used to wring the most money out of our pockets, such as the upcoding industry and tacking facility fees onto visits.

As the saying goes, if you're sitting at a poker table and you can't figure out who the sucker is, it's you.

Over the past twenty years, the notion of "consumer-driven" health care has caught on, based on the premise that we'll spend heath care dollars more effectively if we use more of our own money. We're certainly now paying more in premiums and in deductibles. The average deductible for the cheapest ACA plans in 2017 are over $6,000. Employer-plan deductibles aren't quite as high, but also have been rising rapidly.

In response, an entire industry has developed around "transparency tools," which attempt to help consumers comparison shop based on cost and quality. Companies like Castlight Health, Healthcare Bluebook, and GoodRx have sprung up to address the need for better information. Indeed, United Healthcare reported last year that nearly a third of consumers had comparison shopped, up from 14% in 2012.

The trouble is that there doesn't seem to be much evidence that such comparison shopping works.

Health Care Cost Institute estimated only 43% of health care services are "shoppable," further noting: "There is not that much savings to be gained from consumer shopping for many non-emergency services." Studies published in JAMA and elsewhere seem to confirm that use of transparency tools have little discernible impact on spending.

Despite the lack of evidence, requiring providers to post more prices has been a favorite legislative tactic, including the Affordable Care Act and in numerous states. The HCI3-Catalyst for Health Payment Reform scored the latter, and only awarded 3 states with "A"s for their efforts; 43 states received "F"s.

Ohio is an example of a state that passed a tough law, requiring providers to provide patients with a "good faith" estimate of what patient's (non-emergency) services would cost, after insurance. As Kaiser Health News reports, it was passed two years ago but still has not gone into effect, facing legal and other opposition by a wide range of provider organizations. They claim the information is too difficult to obtain, and better provided by insurance companies.

Ohio is an example of a state that passed a tough law, requiring providers to provide patients with a "good faith" estimate of what patient's (non-emergency) services would cost, after insurance. As Kaiser Health News reports, it was passed two years ago but still has not gone into effect, facing legal and other opposition by a wide range of provider organizations. They claim the information is too difficult to obtain, and better provided by insurance companies.

The problem is two-fold: providers could more easily provide an estimate of their charges, which would in most cases would be both embarrassing (because they'e so high) and meaningless (because few people actually pay them), and prices vary dramatically both between health plans (based on their negotiated prices) and even between within a health plan (based on network/plan design).

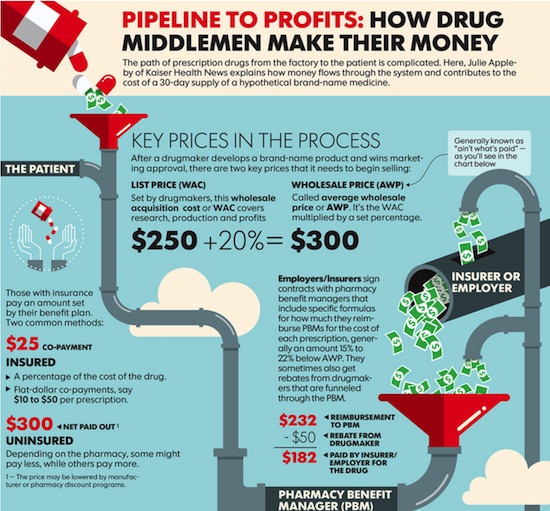

There are no real prices in health care, and here's an example of why:

If you don't understand the graphic, don't worry: the parties involved in it don't intend for you to. It happens to be for prescription drugs, which have a distinct set of players, but it would be easy to do similar graphics for other parts of the health system. You're not intended to understand any of the pricing.

It's as if Amazon based your prices on when you were shopping, where you lived, who you worked for, what device you were shopping on, and which credit card you used. And even then you'd find the pricing results might vary 10x or more between sellers, leading you to wonder if what you were buying was the even same thing.

In a health care system where we can't even figure out what prices are now, it shouldn't be surprising that health care prices rise quickly, because who can tell?

In theory, the prices our health plans negotiate ostensibly on our behalf should mitigate providers' price increases, but that doesn't seem to have happened. Critics claim that having predictable provider prices is more important to health plans than having lower ones, since as premiums rise so can their profits. That's probably not entirely fair, but it is fair to say that neither providers nor health plans have focused enough on making care affordable for consumers.

In an article in The Wall Street Journal (which was the source for the kangaroo joke), Andy Kessler notes "the high cost of raising prices," claiming: "The more prices rise, the more customers bolt." He cites the U.S. Postal Service, movie theaters, and ESPN as examples.

Mr. Kessler points out that GE's former CEO Jack Welch preferred costing costs, adding features, and improving service to raising prices, telling subordinates: "any idiot can raise prices." .

Evidently there are a lot of idiots in health care.

Our crazy-quilt system of health care pricing cannot last. It's costing us too much and not delivering the results it should. We may end up with single payor (or, as Dan Munro suggests, single payor pricing). Or, new entrants will steal the market.

Mr. Kessler says: "Increasing prices attracts others to attack your market... Investors love protected businesses, but eventually relentless price increases kill them all" He specifically quotes Amazon's Jeff Bezos, " Your margin is my opportunity," and it certainly is no coincidence that Amazon is increasingly rumored to be moving into health care.

It may not end up being Amazon that disrupts health care, or it may not end up being only Amazon, but it will end up being someone.

We deserve to be treated better than that kangaroo.

| Kangaroos, Insurance Companies, and the Rising Cost of Healthcare was authored by Kim Bellard and first published in his blog, From a Different Perspective.... It is reprinted by Open Health News with permission from the author. The original post can be found here. |

- Tags:

- affordability

- Amazon

- Andy Kessler

- Castlight Health

- comparison shopping for healthcare

- consumer-driven health care

- Elizabeth Rosenthal

- Gerry Anderson

- GoodRx

- HCI3-Catalyst for Health Payment Reform

- Health Care Cost Institute

- Healthcare Bluebook

- healthcare prices

- Jack Welch

- Jeff Bezos

- Kaiser Health News reports

- Kim Bellard

- national healthcare spending

- Ohio

- Patient Protection and Affordable Care Act (ACA)

- quality of care

- transparency

- United Healthcare

- Login to post comments